New York Administrative Law Judge Approves “Drop-and-Swap” At Closing

New York Administrative Law Judge Approves “Drop-and-Swap” At Closing

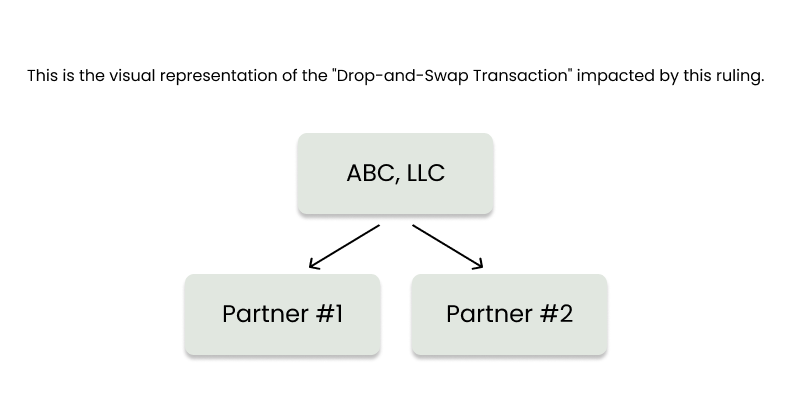

On June 12, 2025, the New York Division of Tax Appeals issued a favorable opinion confirming that “at-closing drop-and-swap” transactions can qualify for Section 1031 nonrecognition—even when real estate is distributed to partners and exchanged immediately afterward.

What This Means:

Traditionally, tax advisors have often recommended complex or time-consuming strategies (such as holding property for several months) to help ensure tax deferral under Section 1031 after a property is distributed from a partnership.

This new decision confirms that no specific holding period is required under Section 1031. It also upholds the ability of taxpayers to complete exchanges immediately after receiving undivided property interests from a partnership. It also may reduce the need for cumbersome or expensive structures previously used to defend these transactions

“There is no authority for the proposition that title to the property must be held for more than one day... [A] similar argument was rejected by the court in Bolker v. Commissioner.” “Thus, the . . . interpretation that the 'held for' language of IRC (26 USC) § 1031 requires that the property be held for a 'minimum of a couple of month[s]' or other arbitrary duration is unreasonable and, accordingly, rejected."

Practical Considerations:

The ruling currently applies only in New York state, but its reasoning may be persuasive elsewhere.

The IRS has not formally adopted this position, so careful planning and documentation are still essential.

This development may offer greater flexibility for structuring tax-deferred real estate transactions involving partnerships.